Nestled in the heart of Europe, Luxembourg stands as a global financial powerhouse, defying its modest size. Beyond its scenic beauty and rich history, Luxembourg boasts a unique fusion of expertise, extensive networks, and a thriving private market ecosystem that continues to captivate a discerning business audience. In this article, we delve into what sets Luxembourg apart as a hub for private markets and alternative investment funds while exploring the dynamic interplay between personal networks, expatriate communities, and the flourishing business landscape of the Grand Duchy.

The Grand Duchy’s Formula for Success

Luxembourg’s allure in the world of private markets and alternative investment funds owes much to its regulatory prowess. Operating under a robust regulatory framework, Luxembourg seamlessly combines stability and flexibility, fostering an environment where innovation thrives, and investor confidence remains steadfast. This equilibrium attracts asset managers, private equity firms, and hedge funds seeking smooth access to European markets.

Moreover, Luxembourg’s extensive tax treaty network and EU passporting rights offer unparalleled access to investors and markets across the European Union. This strategic positioning has been instrumental in attracting capital not only from within Europe but also from beyond its borders.

The Power of Personal Networks

While regulatory and logistical advantages are pivotal, Luxembourg’s true strength lies in its interconnected personal networks. In a nation where a thriving expatriate community fosters an environment of opportunity, personal relationships often form the bedrock of business ventures. Business leaders, financial professionals, and entrepreneurs converge in Luxembourg, forging a unique environment where ideas, funds, and expertise flow seamlessly.

These networks extend far beyond Luxembourg’s borders. The Grand Duchy has long served as a melting pot of cultures and nationalities, attracting professionals from around the world. This diverse expatriate and business community cultivates a dynamic setting that transcends international borders.

Navigating the Alternative Investment Landscape

Luxembourg’s prowess in the private markets and alternative investment funds arena is unmistakable. It has solidified its status as a premier domicile for alternative investment structures, encompassing private equity, real estate, and infrastructure funds.

Here are some reasons:

Expertise: Luxembourg boasts a deep multilingual talent pool of professionals with specialized knowledge in alternative investments, from fund administrators to legal advisors, ensuring the expertise required to manage complex structures is readily available.

Global Distribution: Luxembourg’s extensive distribution networks enable fund managers to access a diverse array of investors, a priceless asset in today’s globalized investment landscape where access to capital is paramount.

Efficiency: The country’s efficient regulatory framework, coupled with its cutting-edge fintech infrastructure, streamlines fund operations and enhances transparency, providing investors with robust oversight.

Sustainability: Luxembourg leads in promoting sustainable finance, with the government’s unwavering commitment to ESG (Environmental, Social, and Governance) principles aligning with the global shift toward responsible investing.

The Luxembourg Advantage in Private Markets

Luxembourg’s appeal in private markets transcends access to capital or favorable regulations; it’s the vibrant, interconnected ecosystem that truly sets Luxembourg apart. The Grand Duchy’s private markets industry thrives because of the close-knit relationships that facilitate deal-making and innovation.

The Role of Industry Associations

Luxembourg’s success story in the fund industry is greatly indebted to industry associations such as the Association of the Luxembourg Fund Industry (ALFI), the Luxembourg Private Equity and Venture Capital Association (LPEA), and also Luxembourg for Finance as public-private agency. These associations play pivotal roles in shaping the future of the fund industry in the country. Through their collaborative efforts, these associations have enhanced Luxembourg’s reputation as a top destination for private markets and alternative investments, reinforcing the nation’s commitment to excellence and innovation.

ALFI (Association of the Luxembourg Fund Industry): ALFI has been at the forefront of advocating for the Luxembourg fund industry, celebrating its 35th anniversary in 2023. It provides valuable insights, conducts research, and fosters a collaborative platform for industry stakeholders. ALFI’s initiatives have created an encouraging environment for innovation and growth in the fund sector.

LPEA (Luxembourg Private Equity and Venture Capital Association): The LPEA is instrumental in driving the private equity ecosystem in Luxembourg. LPEA actively promotes knowledge exchange, networking, and the adoption of industry best practices, further strengthening the country’s position as a leading private markets hub.

Luxembourg for Finance: Luxembourg for Finance plays an integral role in promoting the Grand Duchy as an international financial center. It acts as a catalyst for attracting financial institutions and investors while facilitating dialogue between the public and private sectors.

Future Outlook

In the future, Luxembourg remains well-positioned to navigate the evolving landscape of private markets and alternative investments. The Grand Duchy is at the forefront of embracing emerging trends in the industry, including digitalization and the growing importance of ESG criteria in investment decisions. These forward-looking initiatives are expected to further strengthen its status as a leading financial hub with global reach.

Conclusion

In conclusion, Luxembourg’s distinctive blend of expertise, extensive networks, and a thriving private market ecosystem has solidified its global leadership in alternative investments. Bolstered by its deep ties with expatriate and business communities and supported by industry associations like ALFI, LPEA, and Luxembourg for Finance, Luxembourg’s business environment encourages innovation, collaboration, and embraces diverse perspectives.

For sophisticated business and fund professionals seeking an integrated financial platform in private markets and alternative investment funds, Luxembourg isn’t just a location; it’s a strategic nexus where talent, capital, and networks converge. This unique ecosystem continues to shine as a beacon of financial excellence, emphasizing the lasting influence of relationships and industry collaboration in the world of finance.

Thorsten Lederer, with over 25 years of experience in the financial sector, including senior roles at Citigroup and ABN AMRO, currently serves as a Senior Advisor at Trustmoore Luxembourg. Trustmoore is known for its excellence in delivering tailored fund administration and capital markets services. Mr. Lederer’s finance blogs, covering topics such as distressed debt, private equity real estate, and middle-market investing, complement his frequent appearances as a moderator and panelist at private markets conferences.

Report on the Forum Bundesbank event at the head office of the Deutsche Bundesbank in North Rhine-Westphalia on 16 November 2023

The United Kingdom (UK) finally left the European Union (EU) at the end of the 11-month transition period on 1 January 2021. Some observers predicted difficult times for the British economy in the run-up to this and forecast a high migration of jobs from London as a financial centre to the EU, for example to Frankfurt and Paris. Has this happened? How has the British economy developed since then and what are the future prospects for the British economic model post-Brexit and the important financial centre of London?

Johannes Gerling, representative of the Deutsche Bundesbank in London, addressed these and other questions in his presentation at the Deutsche Bundesbank’s head office in North Rhine-Westphalia on 16 November 2023. There is great interest in the topic, as developments in the UK and London are of great importance both for the financial centre of Frankfurt and for the North Rhine-Westphalian economy.

Structure of the British economy and the role of the financial sector

The structures of the British and German economies differ significantly. In order to better understand current developments, some background information should be provided first:

– The British economy in comparison1:

UK Germany (DEU) Population: 66.97 million 84.08 million GDP $3.07 trillion $4.07 trillion GDP per capita $45,850 $48,433

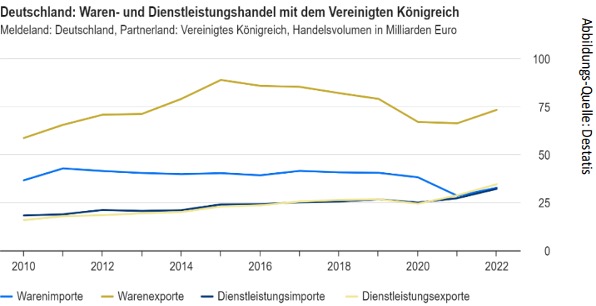

The British economy is significantly less export-oriented than the German economy (GBR approx. 31 %, DEU approx. 48 %)2 and strongly characterised by the service sector (GBR approx. 80 %, DEU approx. 70 %)3 – this is particularly evident in foreign trade (DEU: clear dominance of goods exports; GBR: almost balanced ratio between goods and service exports)

The financial sector is of particular importance to the UK economy (share of value added approx. 8% (e.g. DEU: approx. 4%), jobs in the financial sector approx. 1.1 million, 405 thousand of which are in London).

The EU is by far the most important trading partner for the UK, although its share has been declining for some time (exports 42%, imports 50% of total trade in 2022). A deficit in bilateral trade in goods with the EU of £117 billion contrasts with a surplus of £25 billion in trade in services.

New framework for EU trade relations

Two agreements form the essential basis for new relations between Great Britain and Northern Ireland and the EU:

The Withdrawal Agreement primarily regulates the rights and obligations arising from the UK’s long-standing membership of the EU, including payments to the EU budget. The Northern Ireland Protocol as part of the agreement prevents a “hard border” between Northern Ireland and the Republic of Ireland, but at the same time introduced a new customs border between Great Britain and Northern Ireland. The agreement came into force on 1 February 2020 and provided for a transition period for the UK to remain in the EU single market until the end of 2020.

The trade and cooperation agreement primarily regulates trade relations and fishing quotas, but also cooperation in areas such as law enforcement, justice and research. It was signed on 24 December 2020 and came into force on 1 January 2021. It enables the largely duty-free movement of goods, but does not prevent the creation of new, non-tariff trade barriers (customs documents, product safety certificates, etc.). The free movement of persons between the EU and the UK no longer exists.

Similar to other modern free trade agreements, the trade and cooperation agreement essentially only contains very general agreements on trade in services that hardly go beyond the level of the corresponding WTO standards (World Trade Organisation). In the area of financial services, the UK is basically treated like any other third country. A corresponding equivalence decision by the EU, which would form the basis for EU-wide market access, currently only exists in the area of central counterparties (CCPs)4. The financial market dialogue newly established between the EU and the UK does not conceptually go beyond the EU’s exchange formats with the USA and Japan, among others, and does not decide on market access issues.

After Brexit was finalised, relations were initially severely strained as the British government refused to implement the Northern Ireland Protocol agreed with the EU, including new customs controls between Great Britain and Northern Ireland, in accordance with the treaty. An important step towards normalising relations between the EU and Great Britain is the “Windsor Framework” from February 2023, as it addresses some of the key issues surrounding the Northern Ireland Protocol:

Trade and customs issues: Establishment of so-called “Green Lanes” for goods that remain in Northern Ireland (quasi abolition of customs controls), acceptance of GBR standards for food in Northern Ireland by the EU (must bear “not for EU” labelling). Simplifications also for medicines. Parcels to friends and family and from online shops no longer require customs documents. Greatly simplified entry for pets. Specific customs problems for steel are eliminated.

Subsidies and VAT: Restriction of Brussels’ right to have a say on subsidies affecting Northern Ireland. Extensive exemption of Northern Ireland from EU VAT rules.

Sovereignty and institutions: “Stormont Brake” allows the UK to suspend the application of new EU internal market rules in Northern Ireland (EU can respond with “targeted remedial measures”).

There are new foundations for cross-border financial services post-Brexit:

The implementation of Brexit on 31 December 2020 created new conditions for market access in the EU. EU-wide passporting was lost. Instead, EU equivalence decisions and a “patchwork” of national access regulations apply.

The UK granted EU institutions a transitional period of up to three years through the “Temporary Permissions Regime” (even longer in some areas). The EU did not offer any such transitional arrangements for British institutions; these existed or exist in part at national level in the member states. In addition, far-reaching special powers were granted to the British institutions.

In addition, far-reaching special powers were created for the British supervisory authorities (Temporary Transitional Powers) for up to three years in order to be able to flexibly counter possible frictions caused by the on-shoring5 of EU regulations.

Equivalences are the new basis for EU-wide market access, but they do not represent an equivalent replacement for the passporting rights that have been abolished. The EU regulations provide for a total of around 40 sub-areas in which EU-wide equivalence decisions can be made. However, many important regulatory areas are not covered, e.g. credit and insurance transactions or payment services. EU decisions on equivalences are the responsibility of the EU Commission and are unilateral discretionary decisions that are taken in accordance with the priorities of the EU and the interests of the EU financial markets, if necessary with the involvement of the European supervisory authorities, and can be withdrawn unilaterally with a notice period of 30 days.

To date, the EU has been very reluctant to issue equivalence decisions for the UK. There is currently only one EU equivalence decision for the UK, which applies to the UK regulatory and supervisory framework for central counterparties (CCPs).

A joint declaration made by the EU and the UK at the end of 2024 together with the trade and cooperation agreement provided for the establishment of a joint forum for regulatory cooperation in the financial sector. Parts of the British tabloid press therefore expected a downstream “Brexit Deal for the City” with further decisions on EU equivalence at the beginning of 2021. In reality, however, only a framework agreement was reached on the format of a legally non-binding regulatory dialogue similar to the dialogue between the EU and the USA, which provides for an exchange on current regulatory developments, among other things. The granting of EU equivalences, on the other hand, remains a unilateral decision by the EU Commission. The first meeting of the new financial market dialogue took place on 19.10.2023.

Another contentious issue is the extensive use of UK financial market infrastructures for clearing derivatives by financial institutions based in the EU. Temporary EU equivalence for UK CCPs was initially granted until mid-2022, which was necessary to ensure financial stability. The London clearing houses LCH Clearnet and ICE Clear Europe have been categorised as “systemically important” (regulatory indicator Tier 2) by the European Securities and Markets Authority (ESMA). This means that they are subject to ESMA’s direct supervisory powers and the direct applicability of the European Market Infrastructure Regulation (EMIR). The EU Commission is endeavouring to reduce the EU’s excessive dependence on third-country CCPs. The “EMIR 3.0” reform currently being negotiated in Brussels provides for further instruments to reduce existing dependencies. The future of derivatives clearing by EU institutions via UK CCPs is currently still unclear.

Brexit is already leaving its first traces in the British financial sector

London will remain an important global financial centre even after Brexit. The City is still one of the top three leading global financial centres (behind New York). However, competition from the Asian centres of Singapore, Hong Kong and Shanghai is becoming stronger. In Europe, London can build on its strengths: Language, geographical location, metropolitan area, financial expertise, global role of the law of England and Wales, attractive city. However, London’s importance for the EU is likely to continue to decline.

According to estimates, Brexit has already led to the relocation of around 7,500 jobs to the EU – and more are likely to follow. Dublin, Paris, Luxembourg, Frankfurt as a banking centre and Amsterdam in particular are benefiting from relocations. To a lesser extent, there are also new branches of EU institutions in the UK.

Brexit has also led to the relocation of financial assets totalling more than £1.3 trillion. With the completion of Brexit at the beginning of 2021, trading in European equities has largely left London and Amsterdam has become the most important European equity trading centre. Derivatives trading has also seen a significant migration of trading volumes from London to trading centres in the EU and the US.

Starting points for strengthening London as a financial centre post-Brexit:

Establishing London as a leading green financial centre.

Expanding the leading role in the FinTech sector.

Reviewing the domestic regulatory framework to ensure its attractiveness as a global financial centre.

At the same time, utilising the new freedoms of Brexit to better adapt regulation to the needs of the domestic market.

Financial diplomacy: Increased focus on growth markets, particularly in Asia, envisaged financial sector agreement with Switzerland and attempt to maintain British influence in international bodies.

By way of comparison, Germany is also pushing to establish itself as a sustainable financial centre and FinTech location, for example through the German financial centre initiatives (Berlin, Frankfurt, Hamburg, Munich, North Rhine-Westphalia and Stuttgart), as well as in Germany Finance, the working group of German financial centres.

Current development of the British economy

New trade barriers as a result of Brexit mean a high level of bureaucracy for exporters and importers, particularly due to customs declarations and accompanying documentation requirements. This is a particular burden for SMEs. Some are withdrawing from previous business with European partners.

Pandemic and energy price crisis overshadow the impact of Brexit. Economic development in the UK is roughly analogous to that in Germany. In other words, external factors such as the pandemic and the energy price crisis are dominating macroeconomic development (in DEU and GBR alike) and overshadowing the macroeconomic effects of Brexit. Gross domestic product also slumped significantly in the UK in 2020. The unemployment rate rose sharply in 2020/2021 and recovered in 2021/2022; it remains noticeably higher in the UK than in Germany.

Similar to the eurozone, the UK has recently been plagued by high inflation. As in the eurozone, the main drivers of inflation were disruptions to global supply chains, a sharp rise in energy prices, high private savings during the pandemic and pent-up demand for consumer goods. The situation on the labour market is tense and there is a shortage of skilled workers in many sectors. The sharp rise in inflation has prompted the Bank of England to make 14 interest rate hikes in succession between December 2021 and August 2023; at the last three meetings, the Bank of England left the base rate unchanged at 5.25 %.

However, inflation has been particularly stubborn in the UK so far. Core inflation and services inflation – as indicators of price pressure from the domestic economy – are well above the eurozone level. One important reason for this is friction on the British labour market:

The UK’s trade with the EU is suffering as a result of Brexit. Trade with Germany is also weak:

Trade with the UK has become less important for Germany. According to Destatis, the UK was still Germany’s fifth most important trading partner in goods trade in 2015 – in 2022, it was only in 11th place. However, Germany still has the third largest foreign trade surplus with the UK. However, the interpretation of the trade data is complicated by a number of special effects, including statistical ones.

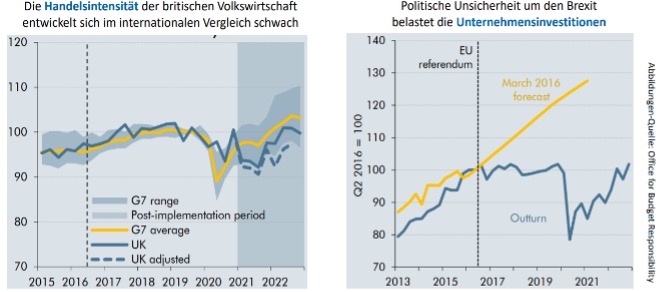

Reduced trade intensity and weak corporate investment are weighing on growth potential:

Most studies assume that Brexit will reduce the UK economy’s production potential by around 3 to 5 % in the medium term compared to where it would be without Brexit. However, quantifying the effects is not easy, partly due to methodological breaks and overlapping factors. The investment ratio, which has been low for years, is also likely to affect the prospects for competitiveness and growth in the longer term.

Expectations of “interesting trade agreements” and expansion into new markets have tended to be disappointed. New agreements that did not already exist through EU membership were mainly concluded with Japan, Australia and New Zealand; the economic impetus is manageable. Negotiations with the USA have made little progress. Relations with China have not developed as hoped. Talks are being held with India. It remains to be seen to what extent this partially deindustrialised country will succeed in rebuilding its own production capacities.

Migration to the UK remains high even after Brexit. An increasing number of non-European immigrants are entering the country via a points system for skilled labour. In view of the tight labour market, fundamental change is difficult.

Conclusion of this analysis

The consequences of the pandemic and the energy price crisis have so far overshadowed the impact of Brexit on the British economy. The adjustment of value chains and the decline in foreign trade are likely to weaken productivity growth in the medium term. A constructive economic policy, including a targeted labour market and migration policy, is likely to become even more important. Although Brexit also offers the UK opportunities, it is currently not foreseeable that these will outweigh the benefits of EU membership. London’s importance as a global financial centre is diminishing for the EU.

In an article on 25 November 2023, the Frankfurter Allgemeine Zeitung (FAZ) saw “A divided relationship (of the UK) to globalisation. The UK’s policy is wavering between opening up and cutting itself off. Since Brexit, trade policy has only progressed in small steps.”

However, in the longer term and in view of the geopolitical challenges, there is an opportunity to revitalise economic relations between the EU and the UK on the basis of many shared values.

1Data source: World Bank data for 2022

2Exports measured in terms of gross domestic product (GDP). Sources: Office for Northern Statistics ans Destatis; Deutsche Bundesbank; 2019 before the effects of the pandemic and the implementation of Brexit.

3Contributions to gross value added in 2019. Sources: Office for National Statistics and Destatis.

4CCPs act as financial market infrastructures between the original counterparties of a financial market transaction and replace them. They assume the default risk and thus make a significant contribution to risk management and efficiency.

5On-shoring here: short-term transfer of regulations previously governed by EU law into UK law.

(PHOTO: Kick-off Event FINANZPLATZ DEUTSCHLAND-INITIATIVE of the Börsenzeitung on 13.09.2023 with Hubertus Väth, H.-Joachim Plessentin, Hans-Jürgen Walter, Markus Hill)

“FINANZPLATZ FRANKFURT: What challenges do you see for the Frankfurt financial center in the coming year?

Plessentin: Geopolitical developments and the economic and financial environment will continue to have an impact on Frankfurt as a financial center in 2024. Frankfurt is in competition with financial centers such as London and Paris. Strengthening the financial center and financing the sustainable, climate-neutral and digital transformation are of central importance.

FINANZPLATZ FRANKFURT: What did you take away from the Fin-Connect-NRW kick-off event on 18.12.2023?

Plessentin: The Fin-Connect-NRW financial center initiative will enter the scaling phase in 2024. The new office has presented a coherent concept for expanding the financial ecosystem and intensifying the concrete implementation of transformation processes and their financing. The new specialist working groups are also important for this process.

FINANZPLATZ FRANKFURT: Germany Finance: What impetus will be given to strengthen Germany as a financial center and transformation financing in 2024?

Plessentin: The role of spokesperson for Germany Finance, the working group of German financial centers, will rotate to Fin-Connect-NRW for one year from January. It is certainly planned that Germany Finance will commission a new study on transformation financing in 2024. The extent to which participation in international and national presentations is planned remains to be seen.

I wish my colleagues in the German financial center and the Group a good and successful 2024!”

Mr Hill, you supported and moderated the organization of the „Financial Center Frankfurt meets Financial Center Liechtenstein“ event in Frankfurt on 8 November 2023. What was the bridge to the topic of „Family Offices & Fund Boutiques“?

I was able to win Reiner Konrad from FOCAM AG in Frankfurt for a short presentation on the topic of „Family Offices, Fund Boutiques, and Manager Selection“. In Frankfurt, he gave a good overview of the importance of independent asset managers, asset allocation, and due diligence of the „hidden champions“. I suggested this topic because I thought it would be a good addition to the core topic of the event (private label funds & advantages of launching funds in Liechtenstein). The event of the „LAFV Liechtenstein Investment Fund Association“ provided a good framework for an intensive discussion on topics such as Liechtenstein as a fund location (David Gamper and Bruno Schranz, LAFV), the international role of Liechtenstein (Isabel Frommelt-Gottschald, Ambassador I.E.), regulation (Dr. Reto Degen, FMA – Financial Market Authority Liechtenstein) and asset management and private label funds (Ralph Früh).

I was also able to speak to some of the visitors to the event in Frankfurt afterward. One key point was repeatedly mentioned as feedback. Liechtenstein had presented itself as a very focused service provider, also for „small“ fund initiators (asset managers, asset managers, etc.), perhaps this could also be an approach for the fund industry there in 2024. I am neutral in my assessment of jurisdictions for the launch of funds, each location (Luxembourg, Germany, etc.) has its special advantages and its own „fan base“. I see a potential niche for Liechtenstein here, as many KVGs (Switzerland: „fund management company“) outside Liechtenstein are quite restrictive in their selection of potential fund partners as soon as funds do not promise the potential for high fund volume increases quickly right from the start. There is certainly an interesting segment of fund initiators that can be classified exactly between the very small and the very large fund volumes. Perhaps Liechtenstein can gain market share here over the next few years.

FOTO: Thomas Caduff & Markus Hill – „FINANZPLATZ SCHWEIZ trifft FINANZPLATZ LIECHTENSTEIN“ (Bild: www.fundplat.com)

You will be giving a keynote speech at the „Mountain Talks“ in St. Moritz on 12.01.2024 and moderating a roundtable on the topic of „Family Offices & Fund Boutiques“. What points could be of interest here, for example?

I often deal with the topics of fund selection and seed money search on a project basis. I often find it interesting from which directions fund managers are often viewed here. It is not possible to produce an ad-hoc study on such a small scale. I am currently exchanging ideas with a large number of family offices in advance to take another look at the relationships between these market participants. In addition to these results, some „theory pie chart studies“ may also be interesting, and perhaps I will also make some comments there.

The topics of communication (branding), financial education and networking, and the networking of players in the DACH region also seem interesting to me. During my „short survey“ in the run-up to the event, there may be one or two qualitative „thoughts“ that could perhaps provide a new perspective. Incidentally, I often see overlaps here in the assessment of liquid and non-liquid fund concepts. For example, I have already had ample opportunity to get to know a few alternative approaches to the communication behavior of family offices and fund boutiques at various other events in the DACH region this year in preparation for presentations. There are also overlaps because a „double hat“ is often worn. Multi-family offices, single-family offices, and independent asset managers, for example, act as selectors on the one hand, but many also have their products (private label funds) on the other. Many of the event formats in the family office sector also thrive on the fact that many of these addresses with a „double hat“ (for example: Multi-Family Office) are also looking for investors for their products or investments (co-investments, club deals, etc.). The difference to the many classic fund boutiques („non-selectors“) is perhaps that the classic family officer cannot „market their products“, as this does not necessarily fit in with the „trusted advisor“ theme. There is also a debate in the market as to whether a family office should offer its products at all. It’s an exciting field and I’m already looking forward to the discussion on site. To take a brief position here too: I think it’s fine for family offices to have skin-in-the-game with their products (investments etc.), if this positioning is transparent for clients, then this often seems to me to be a signal that certain family office concepts also express the fact that they have in-depth expertise in practice and can also provide real support for investments. It is often forgotten that this form of professional figurehead can also represent a risk: If the address does not deliver the desired results, then a shadow falls over the entire client relationship!

What topics are still on the agenda for you in 2024?

As mentioned above, I have worked intensively with liquid and non-liquid fund concepts over the years. For example, I had the opportunity to moderate two video discussion rounds with Telos and Artis ICM for premium sponsorships of the study „Preferences of institutional investors in real estate and alternative investments“. On the one hand, the results of the study were discussed, and on the other, there was an opportunity to discuss topics such as real estate and infrastructure investments in greater depth. The questionnaires for the current study will also be sent out to institutional investors shortly. The results are likely to be exciting against the backdrop of the significant changes in the interest rate landscape. It remains to be seen whether this year’s investor reluctance will turn into another „run“ on alternatives. (Input, ideas, and suggestions for „AIF & MORE“ are always welcome!) As an economist, topics from the infrastructure sector seem very interesting to me, with many fund concepts focusing on segments such as transportation, energy, and real estate. The focus is always on the eagle eye, and there is also an interface with topics such as „social issues“ and private debt (keyword: „Financial Center Frankfurt meets Private Markets 2024“). I also find these areas interesting from a journalistic point of view because these fund structures have to be communicated in a completely different way due to regulatory requirements, with topics such as branding and professional expertise taking center stage. Financial education and content count, not „primitive“ product promotion.

The topics of „fund selection“ and „seed money search“ will also be with me next year. It is interesting to note that many of the players in the start-ups, VC, and private equity segments can also always be linked to the topic of „family offices & fund boutiques“ – if you want to see these interfaces. I have always greatly appreciated the opportunity to exchange ideas with „real“ experts in this field. I have been involved in the liquid segment for many years due to several product research projects (manager selection, „reality check fund concept“ & investor dialog, etc.), in the non-liquid segment I am often more of a „humble learner“ – but with an increasingly steep learning curve. To pick up on the topic from above (Liechtenstein): the topic of „liquid versus non-liquid investments“ and fund launches also often comes up in these discussions.

Looking forward to the talks at the „FONDS professionell KONGRESS“ at the end of January 2024 in Mannheim and various other participants (presentations, moderations, media partnerships, etc.) in the DACH region. I will also continue to focus on the topic of „India“, hopefully, a small farewell party will also work out in February at the financial center in Frankfurt with an industry colleague I greatly appreciate, I would like to give a small speech in his honor, in combination with another topic. Here I have a location with a distant „India background“ in mind, so to speak „Financial Center Frankfurt says FAREWELL!“ in a small circle. I won’t lose sight of the topic of „Liechtenstein“ either; I still have an interview to do here. In connection with such activities, I would like to „optimize“ my activities on LinkedIn next year. Connecting the topic of the financial center (LinkedIn channels „Financial Center“: Frankfurt, Germany, Switzerland, Liechtenstein, Austria) always opens up new opportunities for me to exchange professional ideas. One new development in 2023, for example, was the activation of a „Financial Center Frankfurt am Main Group“; by the end of January, we should have exceeded the 1,000-follower mark. The group is a good addition to the Finanzplatz Frankfurt am Main channel (community, target for the end of January 2024: 7,500 followers). I think that the next year offers a good opportunity to network with the various financial centers in the DACH region more closely via LinkedIn. Thank you for your support in 2023, by the way!

Markus Hill has been an independent asset management consultant since mid-2005. His professional background includes companies such as SEB Bank (marketing/product management, investment banking) and Credit Suisse Asset Management (sales, asset management). His areas of activity include the management of mandates in marketing, PR, and fund selection. As former Head of Sales of mutual funds at an investment boutique (equities and bonds) and in external cooperation with a fund of funds manager, his focus is on small to medium-sized asset management companies. In addition, his journalistic work focuses on the topics of fund boutiques (fondsboutiquen.de) and the use of mutual funds by institutional investors as well as the selection of target funds in multi-management approaches. He is also interested in the financial center Frankfurt as a place for the exchange of ideas (finanzplatz-frankfurt-main.de).

„One should be absolutely wary of predictions, especially those about the future“ (Mark Twain). Markus Hill spoke on behalf of FONDSBOUTIQUEN.DE with Michael Heise, publicist and chief economist of HQ Trust, about the connection between the fields of economics and family office as well as the challenges for investors in the current interest rate environment. Topics addressed included the ECB, interest rate policy, inflation and the implications for capital market returns. These topics, as well as the topic of alternative investments, will also be the focus of discussion this week at the Private Wealth Forum Germany and the Private Debt Investment Forum in Munich.

Hill: As an economist, where do you actually see the connection to the topic of „Family Office & Asset Allocation“?

Heise: Advising families on how to secure and increase their assets is an extremely exciting task. In my view, it is closely linked to global economic developments, which play a major role in determining long-term trends on the financial markets. In this respect, a passion for economics is a good prerequisite for advising family offices. For economists working in the financial business, which has been the case for me since 1995, the special challenge is not only to present academically interesting analyses, but also to generate instructions for action for investors. And they are, as you know, subject to the merciless judgment of the markets. That’s what makes the work so exciting.

Hill: Why do you think the ECB has been so late in responding to inflation?

Heise: The sudden rise in inflation in recent years has surprised the vast majority of forecasters in its rapidity. However, this is no excuse for the central banks. The European Central Bank, in particular, held on to the thesis that the rise in inflation was only temporary for far too long, so it took countermeasures very late. The ECB’s first interest rate hike took place in July 2022, when inflation had already reached almost 9%. How did this late reaction come about? Of course, it can be argued that our forecasting models do not work so well in times of massive shocks such as the COVID pandemic and the Ukraine war. More importantly, the European Central Bank had just revised its strategy in 2021 and a very expansionary policy stance emerged. As late as the end of 2021, the ECB announced a long period of low key interest rates as part of its so-called forward guidance, thus shaping market expectations. This assurance then prevented it from raising interest rates in a timely manner. In doing so, it would have undermined its own announcements.

Michael Heise, Chief Economist, HQ Trust GmbH

Hill: What’s next for inflation and the ECB’s key interest rate?

Heise: In my estimation, the ECB’s key interest rates will remain at the level they are at now until early summer 2024. In view of the weak economy in the euro zone and the fact that inflation figures are falling, the ECB is unlikely to tighten monetary policy further for the time being. Of course, the decisive factor is the development of inflation. Significantly rising commodity prices or aggressive wage increases could change the picture.

Hill: What are the implications for capital market yields?

Heise: With the current direction of monetary policy, capital market yields are likely to move more or less sideways at current levels. Significant interest rate cuts by the central banks would only be expected in the event of a stronger recession, which most forecasters do not currently see coming. So I don’t think you should position yourself for falling interest rates.

Hill: We had a preliminary discussion about our panel at the Private Wealth Germany Forum in Munich. What other topics are important to you there?

Heise: It will certainly be a very interesting panel. I’m particularly looking forward to discussing different scenarios. What is the likelihood of a recession, a severe economic downturn? A recession scenario would have very different capital market implications. I assume that opinions differ here.

Hill: What additional issues are you currently facing?

Heise: This week is all about alternative investments. On October 18, I will be giving a keynote at the Private Debt Investment Forum 2023 here in Munich. Private debt investments have developed very strongly recently and have attracted high demand. However, they are also affected by macroeconomic developments and risks. There’s a lot to discuss there.

Hill: Thank you very much for talking to us.

Michael Heise has been an independent consultant and publicist since 2020, as well as chief economist of the asset manager HQ Trust GmbH in Bad Homburg. He studied economics at the University of Cologne and earned his doctorate. His professional career led him via the German Council of Economic Experts (Sachverständigenrat zur Begutachtung der gesamtwirtschaftlichen Entwicklung) and the positions of Chief Economist at DG Bank and DZ Bank to the Allianz Group in Munich. Heise is an honorary professor at Goethe University in Frankfurt.

PRIVATE WEALTH GERMANY MUNICH FORUM (MUNICH, 17.10.2083):

PRIVATE WEALTH, FAMILY OFFICES, ECONOMICS & Finanzplatz Deutschland (München, 17.10.2023) – „Panel Discussion: Fixed Income: Rising Trends Shaping Today’s Landscape Inflation is at its highest rate in four decades. Central Banks may continue to raise rates. Given this precarious moment in time, investors are left wondering if the 60/40 portfolio is still viable, in light of correlations between stocks and bonds. This panel will aim to answer such key questions as: • How much higher will the ECB raise rates and how quickly could they cut rates? • How will the ECB reduce its balance sheet and for how long? • How is liquidity in the bond market and what is the impact on fixed income portfolios? • Could this be a year with bonds and stocks up? How does that affect investing behavior of clients? Moderator: Markus Hill, Managing Director, MH Services – Panelists: Martin Friedrich, Head of Economic & Market Research, Lansdowne Partners Austria – Michael Heise, Chief Economist, HQ Trust – Timur Shaymardanov, Senior Product Specialist -Xtrackers Index Strategy & Analytics , Xtrackers by DWS – Dr. Wolfgang Bauer, CFA, CAIA, Fund Manager, M&G Investments

The 6th Annual Private Wealth Germany Forum is the region’s leading conference for family offices, high net worth wealth managers and private banks from throughout the region and one of the flagship meetings of our global private wealth series. The forum’s content was developed through hundreds of one-on-one meetings with the HNW family wealth management community and the program’s speaker faculty is primarily comprised of leaders in the sector from across Germany.“ (QUOTE – Markets Group – www.marketsgroup.orgVanessa Orlarey)

PRIVATE DEBT INVESTOR GERMANY FORUM (MUNICH, 18.10.2023):

“09:00 Keynote: Economist

Factors influencing credit macro conditions.

Dr. Michael Heise, Chief Economist, HQ Trust/ Macroadvisors”

“On 17-18 October in Munich, the Private Debt Investor Germany Forum will connect the most influential asset allocators and funds from the DACH region and beyond. Over 60 institutional and private investors will come together to meet private debt fund managers and the wider market to learn about the latest trends, explore investment opportunities and decide where to allocate their capital. Attendees will hear from over 70 speakers across the forum and have many opportunities to connect with active investors in Germany, Austria, and Switzerland. Join your peers at the Germany Forum for an unmissable two days of content and networking in the region.

„Financial Centre North Rhine-Westphalia“, Financial Centre Frankfurt, Economy, Innovation, Germany Finance & Cooperation of Financial Centres – Markus Hill spoke for FINANZPLATZ-FRANKFURT-MAIN.DE about these topics with Heinz Joachim Plessentin, former coordinator of Fin.Connect.NRW at the Ministry of Economics of NRW. Further components of the discussion were additionally the areas of venture capital, ESG, and transformation as well as the contents of the study „Germany as a financial centre as a cornerstone of the European financial system“.

Hill: Fin.Connect.NRW has attracted attention beyond the state borders. Compared to other financial centres such as Frankfurt, the financial centre initiative is still relatively young. What are the special features, what is the unique selling point of Fin.Connect.NRW?

Plessentin: Indeed, the structures in North Rhine-Westphalia are special. The state has a rather decentralized organization with several major centres such as Düsseldorf, Cologne, and Münster. North Rhine-Westphalia is Germany’s second-largest banking center after Frankfurt, with a focus on Düsseldorf. Next to Munich, Cologne is the strongest insurance location. The state is an important location for industry, medium-sized businesses, and science. Accordingly, Fin.Connect.NRW is not a city-based initiative, but an overarching state initiative that brings together all the players. Fin.Connect.NRW is the financial centre initiative focusing on sustainable, climate-neutral, and digital transformation and its financing. We also have the classic financial center topics on the agenda: location marketing, human resources, innovation & fintech. For example, InsurLab Germany in Cologne is the largest industry initiative to promote digitization and innovation in the insurance industry.

Heinz-Joachim Plessentin, Fin.Connect.NRW & Markus Hill

Hill: For a financial center initiative, the ecosystem and networking are crucial. Networking is essentially based on contacts in the financial industry and the business sectors, personal trust, and mutual appreciation. Who is on board as a cooperation partner in Fin.Connect.NRW?

Plessentin: Fin.Connect.NRW will further expand NRW’s financial ecosystem, especially given the major economic challenge of transformation. The competitiveness and performance of a financial center and sustainable finance in the broader sense depend to a large extent on the performance of the ecosystem. We „span the arc“ from science to finance to the „real economy“. The real economy is represented by the NRW Chamber of Industry and Commerce, the credit industry associations, and the NRW headquarters of the Deutsche Bundesbank are also founding members. Furthermore, in addition to the insurance industry, the stock exchange, private equity companies, NRW.BANK, the Center for Innovation and Technology in North Rhine-Westphalia, or ZENIT for short, the Institute of German Business and the Institute of Energy Economics at the University of Cologne, bank and business professors, and consulting firms such as BCG and zeb are part of the initiative.

Hill: That’s impressive. Who is coordinating the initiative?

Plessentin: We see diversity as a strength. Fin.Connect.NRW is primarily about the topics. The structures are still developing. At present, coordination lies with the Ministry of Economic Affairs, SMEs, Climate Protection and Energy of the State of North Rhine-Westphalia, specifically with my colleague Dr. Dirk Schlotböller and myself in particular. In line with the Future Contract for North Rhine-Westphalia (coalition agreement), Fin.Connect.NRW is being strengthened. On June 14, 2023, the state parliament of North Rhine-Westphalia resolved to strengthen the Fin.Connect.NRW financial center initiative. Specifically, the state parliament has instructed the state government to strengthen the financial center initiative Fin.Connect.NRW and the networking between stakeholders such as companies, the credit industry, insurance companies as well as other players. On this platform, the players are to be able to offer tailor-made financing instruments for syndicated financing with several lenders and to mediate partners. A comprehensive information campaign is to be developed to raise awareness of Fin.Connect.NRW among the relevant target groups. The first NRW climate protection package adopted by the cabinet also includes strengthening Fin.Connect.NRW by awarding it an office, which will start work on November 1, 2023.

Hill: I would like to ask you to elaborate on the conceptual cornerstones. Is diversity a strength of the financial centre?

Plessentin: Yes, we are convinced of that. A study by Germany Finance and Zeb (study entitled „Germany as a financial center – a cornerstone of the European financial system“, in cooperation with the Chair of Banking and Financial Services at the University of Hohenheim, Prof. Burghof, on which I was involved) proves that diversity is an advantage and a strength of the financial system: The German financial centre is an excellent fit with the decentralized, medium-sized economic structure and German federalism. The structures of the economy and the banking sector are very similar. Our financial center consists of several leading regional financial centers with different focuses. This corresponds to the well-known structure of the German real economy, which is diverse, high-growth, international, and stable. New challenges have to be mastered. A diversified economy has a good chance of doing so. The sustainable transformation of the economy – the megatrend of the 21st century – and its financing require a departure and massive innovation, investment, and funding. To explain: Fin.Connect.NRW is a founding member of the Germany Finance working group, along with Frankfurt Main Finance, Finanzplatz Hamburg, Stuttgart Financial, and Finanzplatz München Initiative (with observer status); Berlin Finance Initiative was added. The participating organizations have thus initiated a joint platform to further promote continuous exchange among each other and to provide a central point of contact for people from Germany and abroad interested in Germany as a financial centre.

Hill: How does the cooperation at Germany Finance work? I ask this also against the background that I know and appreciate Frankfurt very well, come from NRW/Cologne, and know that cooperation between countries, financial centres, and organizations is often not that easy.

Plessentin: The cooperation at Germany Finance works well and collegially. This year, the spokesperson role is in Frankfurt, and 2024 it will be with Fin.Connect.NRW. As Germany Finance, we have achieved a lot together with studies on the financial centre, the fintech location, sustainable finance, and in the spring with the consultation on the attractiveness of the financial sector for young people. The cooperation also works well at Fin.Connect.NRW.

Hill: Experience, overarching expertise, and trust built up over the years are essential for coordinating a financial center initiative. My talks, as you know, are therefore about the cause and the people. You are an employee of the Ministry of Economics of North Rhine-Westphalia, were previously with DZ Bank, have dealt with corporate loans and equity financing, funding, and supervisory issues, and are also an author on these issues. What are your personal experiences and assessments?

Plessentin: In the Ministry of Economics of North Rhine-Westphalia, I am involved in the policy department, which deals with issues relating to the future. Coordination and development of Fin.Connect.NRW are therefore not my only task; I also deal with the fundamental issues of the capital and financial markets. My professional experience at renowned institutions (DZ Bank and KfW by today’s name) helps me in this. In addition, the experience I have gained from providing expert support in top-level meetings, in chairing working groups at the federal and state levels, with the departments in the preparation of development bank committees, and with the business community also helps. I have a degree in business administration and am considered a „veteran“ of the financial centre.

Hill: This has shed light on the framework conditions of Fin.Connect.NRW and your coordination, which are essential for understanding. The successes so far are impressive. Nevertheless, more resources and more flexibility are needed for this ambitious task in a scale-up phase. Now to the brand core. The focus of Fin.Connect.NRW is on transformation financing. What does that mean in concrete terms?

Plessentin: The Institute of the German Economy in Cologne has estimated the investment required for climate-neutral and digital transformation at 70 billion euros per year for NRW alone (IW report „Transformation in NRW. How can the digital and climate-neutral transformation of companies in NRW best be financed?“). Of this, climate-neutral transformation accounts for 50 billion euros. This includes both additional and replacement investments. From today’s perspective, the figure is more like 80 billion euros p.a. The majority will have to be financed privately. The banks cannot handle this alone; better use must also be made of the capital market. The challenge in transformation financing is often to better match capital supply and demand. The IW report outlines recommendations for action. The state government and Minister Neubaur have set the „Joint Project Climate-Neutral Industrial Region“ as their goal. North Rhine-Westphalia is to become the first climate-neutral industrial region in Europe and a pioneer on the road to climate neutrality. Fin.Connect.NRW is intended to bundle the forces for the transformation. Fin.Connect.NRW can initiate new solutions. The contribution of the financial sector and companies on this path to the future is of great importance.

Hill: Indeed, the challenges are great right now. Sustainability, climate neutrality, and digitalization are crucial for the financial industry and companies. Business models must be transformed, products and processes adapted, and ESG criteria given greater consideration. How can Fin.Connect.NRW, with its limited resources, contribute to this.

Plessentin: In the start-up phase of Fin.Connect.NRW, the IW’s report was important. It was commissioned jointly with the banking industry associations and quantified the investment and financing requirements for the transformation in NRW for the first time. The financial sector and companies would be well advised to take advantage of the opportunities presented by the transformation. A survey shows that larger companies have opportunities for their competitiveness „on their radar.“ For small and medium-sized enterprises, there is often a need for information. Fin.Connect.NRW, therefore, organizes solution-oriented events together with its cooperation partners to bring together different players across the board, raise awareness, provide practical information, and impart knowledge. The website and the quarterly newsletter also serve this purpose. We are pleased that these offerings are well received. In the future, it will be important to further intensify matching together with our partners to advance the financial center, the transformation of companies, and their financing.

Hill: You are often in Frankfurt. What do you appreciate about Frankfurt?

Plessentin: Frankfurt is the largest German banking center and is internationally positioned. The cooperation with colleagues is good and I get together to exchange ideas. And it’s only a stone’s throw from the Rhine to the Main.

Hill: Finally, a personal question: How long will you continue to coordinate Fin.Connect.NRW? Will you continue to contribute your diverse experience and expertise?

Plessentin: My term of service at the NRW Ministry of Economic Affairs ends on July 31, 2023, so I would like to take this opportunity to thank my colleagues and cooperation partners for their trust and constructive collaboration. I enjoy the topics, the network is pronounced and I have requests. Let’s have a look.

Hill: Great tasks, an interesting prospects and definitely inspiring. Thank you for the interview.

Over four decades, H.-.Joachim Plessentin has provided important impetus and contributions to the economic policy development of the state of North Rhine-Westphalia in various capacities, contributing his expertise in an advisory and supportive capacity. He coordinated the financial center initiative Fin.Connect.NRW from June 15, 2020 to July 31, 2023, was a long-time employee of the NRW Ministry of Economics and previously a banker at DZ Bank and KfW (current designations), holds a degree in business administration and is an author. The interview was conducted in July 2023.

Europe in general and Germany, in particular, are not taking the easy way out when it comes to shaping a sustainable future. As generally accepted as the UN’s sustainability goals are, as much as the words Ecological – Social – Governance (ESG for short) are on everyone’s lips, the attitudes and actions on how these are to be achieved diverge.

In Germany in particular, there is an immense will to fulfill the goals set in all areas and in the best possible way – technical progress should be egalitarian, democratic, and in line with data protection; the energy turnaround should protect the environment without jeopardizing economic growth. We are trying to solve and overcome the conflicting goals and limits that we inevitably come up against with a great deal of (technical) expertise and even more capital investment.

In the area of digitization and its underlying infrastructure, the ambivalence becomes even clearer. On the one hand, this is a key building block for ESG: be it the replacement of the business trip by a virtual meeting, online access for educational purposes in the countryside, or information on the actions of public authorities freely available on the Internet – to name just three examples. On the other hand, digitization consumes large amounts of resources, be it electricity for data centers or rare-earth for batteries and devices. It also sets new hurdles in social and professional participation and is subject to criticism due to data collection and analysis, especially by (American) large corporations.

Unfortunately, the „solution“ to this tension often amounts to stagnation – regulatory requirements alienate investors, NIMBY (Not in my Backyard) protests prevent or delay critical projects, and processes are not digitized „for data protection reasons. The fact that this ultimately helps neither the climate nor society seems to be of secondary importance.

In Frankfurt, a city that has evolved from a banking capital to the data capital of the EU, the challenge is evident in practice: despite the unquestionable availability of capital, expertise, and infrastructure, the city on the Main is neither at the smart city level (Hamburg) nor among the top startups (Berlin/Rhein-Ruhr/Munich) in Germany, let alone in Europe. The city also struggles with its role as the (world’s largest) Internet hub and important data center location – difficult energy supply, unused waste heat, displaced businesses – to name just a few points of criticism.

Michael Jakobi, contagi Digital Impact Group

The new governing coalition in the city parliament is striving to remedy the situation with a digitization strategy on the one hand and regulatory requirements on the other, and in doing so is taking the operators of the data centers to task, for example on the issue of waste heat. The new Telehouse Datacenter in Kleyerstraße is already a pilot project in which waste heat from the data center is to be used to heat a new development in cooperation with Mainova. However, this – very positive – example is not a one-size-fits-all solution, as the conditions at other locations are far less optimal, not to mention the cost-effectiveness of retrofitting existing infrastructures.

Frankfurt will therefore also have to face the challenge of developing holistic concepts in terms of digitization and digital infrastructure – based on sound data and involving not only the data centers but also a large number of other stakeholders from startups to hyperscaler’s (AWS, Google, Microsoft & Co). The fact that these stakeholders are located in Frankfurt and the entire Rhine-Main area in a geographically very confined yet internationally networked space is an important component here that brings both human and technical advantages. So while corporate servers exchange data with low latency and mainframes enable the use of artificial intelligence, human decision-makers and specialists can physically come together to find solutions.

No one believes that this topic will lose its complexity and importance in the next few years. On the contrary, against a backdrop of dwindling resources and advancing climate change, social inequality, and political tensions, we need digitization more than ever – for greater efficiency and social participation, learner administration, and faster processes in general. The fiber rollout that is finally in full swing, together with 5G and its possibilities to help existing approaches such as IoT, AI, M2M, etc. make a breakthrough, are important building blocks here, as are clouds and applications.

To summarize: Only when data centers and the applications running there are seen as part of a complex ecosystem, as part of social change and the energy transition, and significantly more players are involved, can the promise of „ESG – positive“ digitization be realized. Whether in Frankfurt, Germany, or Europe, this creates a historic opportunity to shape the digital transformation in a humane, climate-friendly, free, and democratic way.

AUTHOR: Michael Jakobi, LL.M. is a consultant and project manager in the field of digital innovation & infrastructure at contagi Digital Impact Group – www.contagi.ch

“In a city like Frankfurt, one finds oneself in a peculiar situation; ever-crossing strangers point to all corners of the world and awaken a desire to travel” (Johann Wolfgang von Goethe). Vienna – Frankfurt – Vienna: Markus Hill spoke for FINANZPLATZ-FRANKFURT-MAIN.DE with Martin Friedrich, Lansdowne Partners Austria GmbH, about his private and professional impressions from 16 years in Frankfurt. Cosmopolitanism, investment banking, family office, fund management and schnitzel are some keywords of the exchange of ideas. (Event announcement SCOPE & FUND FORUM INTERNATIONAL – 8.6. & 16.6.2021).

Hill: Mr. Friedrich, you are Austrian and live in Vienna, but you also know Frankfurt very well. Where does that come from?

Friedrich: Well, I have spent most of my professional life in Frankfurt. I came to Germany in 2002 and worked in the Rhine/Main financial center for almost 16 years. During that time, the city has developed a lot. When my wife and I moved in in 2002, Germany was so badly affected by the international economic slump that it was considered the “sick man of Europe.” I also remember that it was practically impossible to buy anything on the weekend, as most shops closed Saturday around noon. Even many restaurants often were closed on Sundays. Today, Frankfurt is a completely different city. It has become much more open to the world, we have made friends who really come from all over the world. Unfortunately, everything is closed at the moment, but before the lock-down I enjoyed taking part in life in Frankfurt and appreciated not only the opportunities for professional development, but also the sports and leisure activities on offer.

Hill: Why did you originally come to Frankfurt? What later drew you back home?

Friedrich: Before I came to Frankfurt, I had worked in London, for the U.S. investment bank Morgan Stanley. The immediate reason for my move was purely professional: at the time, it was decided that my occupation, looking after fund managers in Germany, could be better handled from Frankfurt. So I followed my job, literally. The situation was not unlike was is happening today due to Brexit, it just took place 20 years earlier. Years later, upon leaving Morgan Stanley, I worked for a multi-family office in Bad Homburg, HQ Trust. Of course, I count the pleasant time I spent there as one of my Frankfurt years, especially since it was also, from a professional point of view, an excellent preparation for the move to Vienna. The primary motivation was, once again, professional: Lansdowne Partners Austria offered me the opportunity to launch my own fund based on the investment strategy I developed.

Martin Friedrich, Lansdowne Partners Austria GmbH

Hill: Where did you like to spend your time in Frankfurt the most? What are your fondest memories?

Friedrich: Three places come to mind: first, of course, we really enjoyed the range of good restaurants; sitting on the terrace of the old opera house on a beautiful summer evening, for example. We also often went to the Austrian restaurant on Weißadlergasse, Salzkammer – it’s just a stone’s throw from Goethe-Haus and serves excellent Austrian cuisine! On weekends, we often hiked the Feldberg; as Austrians, we are automatically drawn to the mountains, it seems. I remember that once every winter, there was always a dog sled race around the Feldberg. I thought that was very nice. Finally, I don’t want to hide the fact that I am a passionate golfer. And the Frankfurt Golf Club – which turned 100 years old in 2013 – is truly a jewel. Standing there on the 18th tee and enjoying the view of the skyline has always been something special for me.

Hill: Thank you very much for the interview.

ScopeExplorer Manager Conferences “After the rally of the past 12 months, the focus of many investors is on equities. No doubt about it: equities belong in every multi-asset portfolio. But which asset classes still belong in it? And most importantly, how much of them? In an interview with André Haertel, multi-asset strategist and portfolio manager Martin Friedrich explains why the Lansdowne Endowment Fund invests in more than 15 other asset classes in addition to equities, and how return and risk aspects are balanced in the best possible way.” (QUOTE: Scope Group, Lansdowne Partners – ADDITIONAL INFORMATION: LINK)

Fund Forum International Virtual Alternative markets outlook in choppy waters – Macro updates, demands and megatrends: what can we expect from global and Europe’s alternative markets ahead of 2021? Economic shifts and key trends that could impact the industry and asset allocations. Moderator: Martin Friedrich, Head of Economic and Market Research and Portfolio Manager, Lansdowne Partners, AustriaRandall Kroszner, Deputy Dean for Executive Programs and Norman R. Bobins Professor of Economics, The University of Chicago Booth School of Business LINK: Fund Forum International Virtual – 16th June, CET 14:00 – 14:30)

Deutscher Stiftungstag, MünchnerStiftungsTag, Virtueller Tag für das Stiftungsvermögen: Three events where the financial center Frankfurt is again represented with professional expertise (examples: DEKA, HELABA, KfW, Stiftung Polytechnische Gesellschaft, DIE STIFTUNG, etc.). Markus Hill spoke for FINANZPLATZ-FRANKFURT-MAIN.DE with Tobias Karow, STIFTUNGSMARKTPLATZ.EU, about topics such as diversification, family office, ESG, digitalization, and reputation management. The topic of insight knowledge management, the alignment of event formats, and the special importance of the Association of German Foundations as a Center of Knowhow were also topics of the conversation. (Additional info / event notes: MünchnerStiftungsTag & Digital – 7/1, 6/7 – 6/11 & 5/12/2021).

Hill: What topics will you be covering at your event?

Karow: We’re looking at the topic of foundation assets 2030, so how foundations are investing their assets today for tomorrow. It sounds trivial at first glance, but many foundations honestly have to set the course, so that they don’t find themselves without decent returns tomorrow. Therefore, we offer suggestions on what should include in the investment guidelines, what the diversification requirement is all about, and what role the business judgment rule could play.

Hill: In your opinion, what should and should not be included in the foundation’s assets?

Karow: It’s impossible to make a general statement like that, but one thing, in particular, pays off from an endowment perspective. Investments that don’t deliver an ordinary return must have a hard time with foundations. After all, it is the ordinary returns that allow foundations to realize their purposes; capital preservation is simply secondary to that. However, many foundations look first at precisely this, which is why many foundation assets are misallocated, with too many low-interest bonds, too few equities, and too few alternatives. What foundations also need to sort out for themselves is the topic of sustainability or ESG. ESG is risk management from a foundation perspective, and it is reputation management. Or would you still donate money to a foundation in the future that cannot tell you that it handles its assets professionally?

Hill: Is there also a link to family offices in your activities in the foundation segment?

Karow: I see the bridge to family offices in the role that family offices take on, which would also be a suitable one for foundations and their managers: that of portfolio controller. Many foundations will hardly be able to actively manage money themselves due to a lack of time and professional resources, but it is possible to keep an eye on asset managers and then change the manager if necessary.

Hill: The German Foundation Day will take place from June 7 to 11, 2021. This year it again offers a very interesting program, and the financial center Frankfurt is also represented with economic expertise (DEKA, HELABA, KfW, etc.). Where do your topics overlap, where do you complement each other’s expertise?

Karow: Indeed, the German Foundation Day (Federal Association of German Foundations) is the largest industry gathering in Europe, and it is rightly the case that foundations and foundation experts head for it first. There are certainly overlaps with our Virtual Day for Foundation Assets, because Stiftungstag naturally also addresses the topic of foundation assets, with prominent figures. Our #vtfds2021 is certainly the less prestigious format, we set the accents on the topic of foundation assets perhaps a bit more on the micro-level. And of course, our format is a free live stream.

Hill: What other interesting formats in terms of knowledge management are there in the foundation sector?

Karow: In terms of pure foundation events, it’s the MünchnerStiftungsTag, which takes place on July 1 and this time is a digital event. The topic here is digitalization and where foundations currently stand post-Corona. In March, we also held the Digital Social Summit, a great event with an excellent program that attracted around 1,000 spectators. The webinars of our event partner at #vtfds2021, RenditeWerk, are also still well attended, which may have something to do with the fact that the format existed before the pandemic and is now enjoying a high level of acceptance.

TOBIAS KAROW: „The MünchnerStiftungsTag, it’s good to have it again. It was the last foundation event we had the pleasure of being a guest at in 2020. This year, on July 1, 2021, the MünchnerStiftungsTag will be held digitally, and the program also has the digital world as a theme. The aim is to discuss how digital day-to-day foundation practice already is and what we remain. We have already found three Digissentials in advance.“

Foundations, asset management, fund primer & ESG, from portfolio manager to passive „portfolio controller“ – Markus Hill spoke for FINANCIAL CENTRE FRANKFURT with Tobias Karow, STIFTUNGSMARKTPLATZ.EU, about the current challenges for foundation managers in managing foundation assets. The importance of the founder’s will, the foundation’s purpose, and investment guidelines were discussed as well as mutual funds, crime fiction, Rollski and gin (EVENT NOTE: VIRTUAL DAY FOR FOUNDATIONS ASSETS – 12.5.2021).

Hill: Why is the foundation’s assets a construction site?

Karow: Many things come together. I always say: „We’ve always done it this way meets low-interest-rate“ which explains everything. In Germany, we have a long tradition of investing foundation assets purely in bonds. Thanks to this love of bonds, about 90 % of the 100,000 or so foundations that existed in this country in 1914 disappeared after the Second World War. This is often forgotten, and in practically all countries where foundations existed, investments are made differently, namely broadly and globally diversified, with the focus on a decent return and not only on capital preservation. The fear of loss unites many foundation managers, but it is not a fear that is goal-oriented. I bought my first share when I was 13, and to date, there have been a few crashes and corrections, but each of these setbacks was temporary, one just had to work on the portfolio now and then. Ordinary income is the most important goal of managing foundation assets, and if it is, then the investment policy of a foundation at 0.0% interest rates in the next decade must look different than it did 10 or 15 years ago. But something is changing, that is already foreseeable.

Hill: What options do foundations have in your eyes?

Karow: Well, foundations can continue to do it themselves, but they, i.e. those responsible, must devote sufficient professional and time resources to make an appropriate decision on the investment of the foundation’s assets. It also includes having obtained all possible information to support this decision, just like a prudent businessman. If I’m unable to manage to do this, and as in the case of capital investment this is very likely, doing it myself is not the first option, in my eyes anyway. Foundations should therefore take the path of delegation, i.e. delegate the task of managing the foundation’s assets to professionals. This changes the role of foundation officers away from active portfolio manager to passive portfolio controller, and for me that fits the times much better than fiddling around with a few stocks here and a few bonds there. Before foundation boards do that, they should rather write proper and up-to-date investment guidelines, because if the framework fits, the room for manoeuvre is then at a maximum.

Hill: You are a friend of fund investment for foundations, and you run the platform www.fondsfibel.de here. Why is that?

Karow: If I delegate the management of the foundation’s assets, then fund investment or the compilation of a fund portfolio is advantageous in my eyes from many points of view. Foundations must comply with the diversification requirement, and they can do this wonderfully through funds by investing in different concepts, styles, and asset classes. But foundations must also follow the founder’s will, which means that above all the purpose must be realized. Accordingly, I look for funds that have a longer distribution history or where income is the focus. Since a lot of information on funds is also available transparently, it is easy to make an informed decision, and control based on this information can be institutionalized. In addition, five fund units and five distributions are easier to account for than countless individual stock and bond positions. For me, fund investment is the most suitable way for foundations for these reasons, but above all, the individual goals of the foundation can be mapped much more granularly with funds. This also includes sustainability, on which every foundation has its own opinion; this must then also be reflected in the portfolio, which can be done well with funds. The investment guideline can state that the foundation only buys Article 9 funds, which will make the foundation portfolio look different. I don’t think it’s feasible for most foundations to do ESG themselves.

Hill: When you are not organizing virtual days for foundations, what drives you?

Karow: As a young father, sport is quite important to me, simply as a balance, I like roller skiing, it’s a nice alternative to running when it doesn’t work out with real skiing at the moment. And then I have time for a crime novel again, do miss writing, but on the other hand, being an entrepreneur is also good yet challenging. Currently, we are blogging and working on a foundation marketplace gin, which already has the name.

Foundation assets 2030: A discussion with Hans-Dieter Meisberger (DZ Privatbank), Thomas Meissner (Stiftung Polytechnische Gesellschaft), Arndt Funken (Aquila Capital).

Eco and green are not everything. Final impulses on the couch on the contemporary management of foundation assets by Harald Brockmann (Mission Central of the Franciscans), Immo Gatzweiler (AXA Investment Managers), Markus Hill (fondsboutiquen.de)

ADDITIONAL INFORMATION / REGISTRATION – VIRTUAL DAY FOR THE FOUNDATION’S ASSETS: www.vtfds2021.de

a) Frankfurt Foundation Database (quote): „There are over 600 foundations with their registered offices in Frankfurt am Main. Foundations are involved in many important social areas in our city: in education and training, in science and technology, in art and culture, in social issues through to assistance for the elderly, as well as in nature conservation and environmental protection.“ – SUPPLEMENTARY INFORMATION: Foundation Database | City of Frankfurt am Main

b) Initiative Frankfurter Stiftungen (citation): The Initiative Frankfurter Stiftung sees itself as a network of people who bear responsibility for shaping the foundation system in and around Frankfurt. It has existed since 1993, and finally as a registered association since 1997. Its members represent the entire spectrum of the foundation sector and represent young and old, large and small, charitable foundations under civil law as well as institutionalised foundations. Members are co-opted. Membership is by name.“ – ADDITIONAL INFORMATION: www.frankfurter-stiftungen.de

VIRTUAL DAY FOR THE FOUNDATION ASSETS (12.05.2021 – www.vtfds2021.de)

„One, two, three, at a whizzing pace time runs; we run with it.“ (Wilhelm Busch). Frankfurt, innovation, resilience, and entrepreneurship – Markus Hill spoke with author Ortrud Toker for FINANZPLATZ-FRANKFURT-MAIN.DE about entrepreneurial personalities, inventiveness, and the historical significance of slowness, speed, and communication. Topics such as technology, inventiveness, and Prussia are addressed as well as data transmission, banking, and Frankfurt’s Paulskirche.

Hill: The Frankfurter Rundschau called your book „Vom Ende der Langsamkeit“ a public favourite, HR2 Kultur and Thalia recommend your book as a „Buchtipp“. Before Lockdown, you had many readings, including at the DenkBar, the Weltenleser bookshop and the Kulturfabrik in Sachsenhausen. What is your book about?